‘Value Annihilation’ Haunts Investors in China Property Bonds

China Credit Tracker

China’s offshore credit market rebounded this week after a key bond regulator expanded a financing support program.

But one of the worst routs ever suffered just last month is making many investors skeptical that the rally will last, after even giants of the property industry previously considered safer were shown to be vulnerable.

High-yield dollar bonds lost 12% in October and investment-grade notes shed 3%, both the second-largest declines in respective Bloomberg indexes going back to 2009. A majority of junk-rated developers traded below 10 cents on the dollar, while some high-grade builders like Longfor Group Holdings Ltd. plunged deeper into distress to new lows under 50 cents.

There’s been “total value annihilation” in property firms’ dollar notes, said Anthony Leung, head of fixed income at Pollock Asset Management Ltd. “The sheer scale of destruction in value will have a profound impact on the investment appetite on all kinds of China risk assets. This loss of confidence will likely be very prolonged, if not permanent.”

Stress for offshore notes remained at the highest level in October, according to Bloomberg’s China Credit Tracker. While stress in the local credit market did climb one step from the lowest level, defaults continue to run far below both recent years’ levels and delinquencies in dollar bonds in 2022.

The property-debt crisis entered a new phase last week as two large developers issued bond-payment warnings. One of them, CIFI Holdings Group Co., was among the first round of firms to sell a yuan note with a state guarantee under a program that emerged in August. The builder’s offshore-bond payments suspension hurt confidence across the market.

Things have gotten so bad that Zhi Wei Feng, a senior analyst at Loomis Sayles Investments Asia Pte who has worked on credit research since 2005 when the first-ever Chinese real estate firm dollar bond was issued, calls that market “no longer analyzable.”

Meanwhile, there have been some signs of risks in the domestic credit market, even as overall it is still largely unfazed.

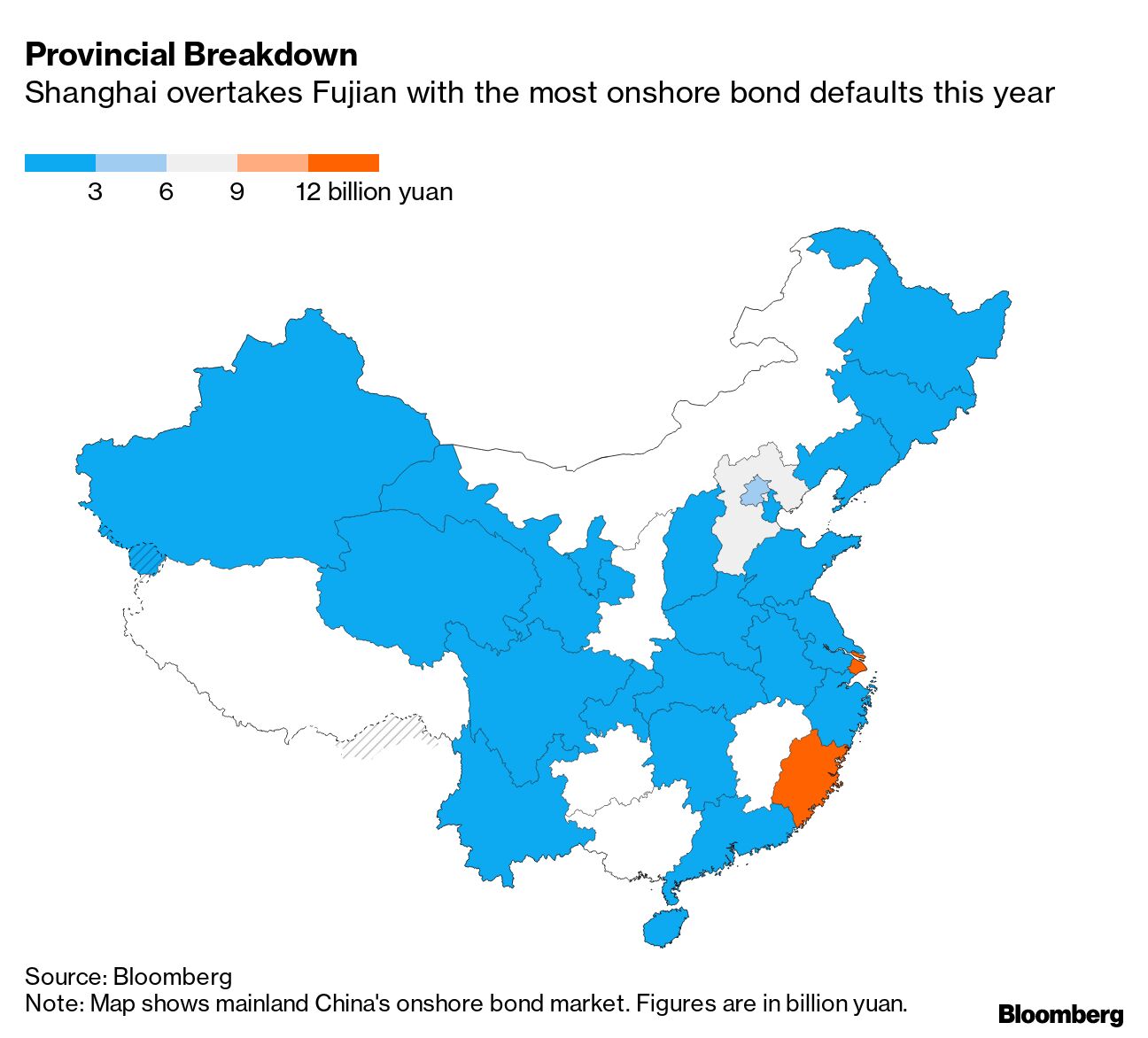

China’s 25th-largest builder by sales, Jinke Properties Group Co., last week became the country’s first new onshore-note defaulter since July.

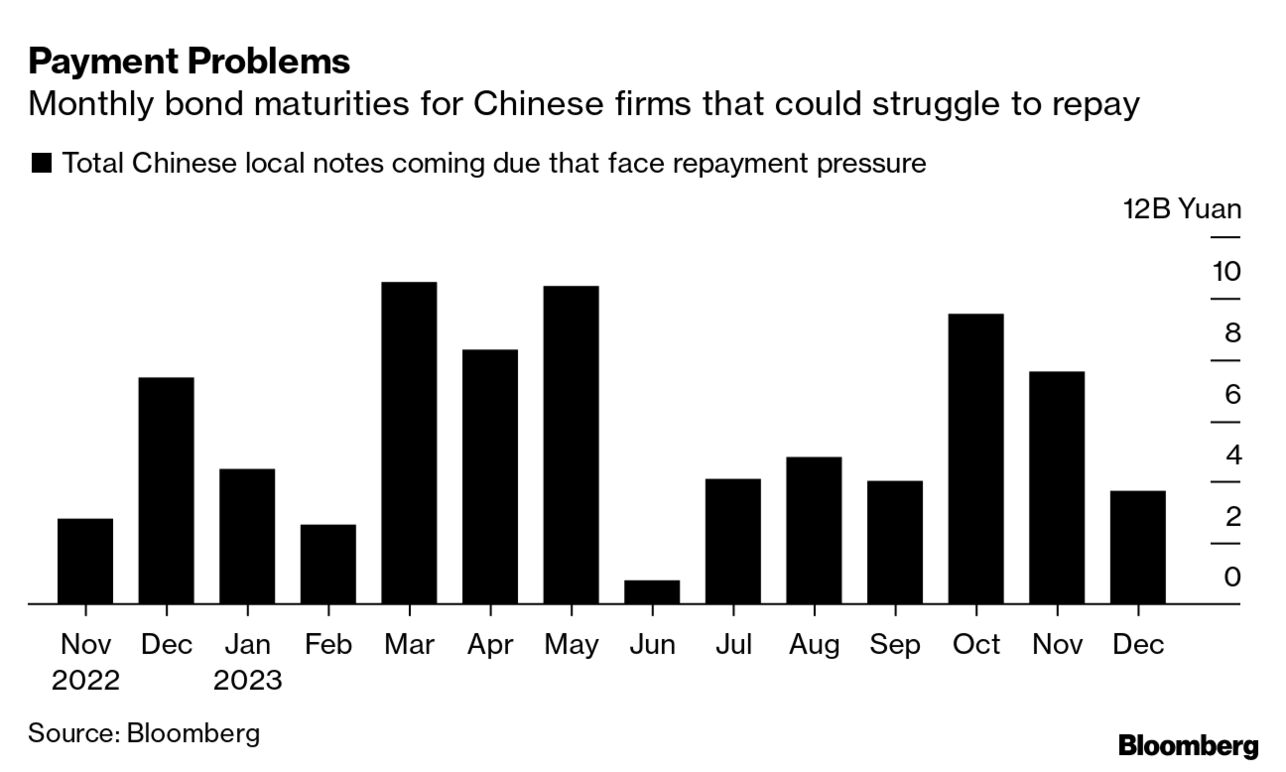

Payment Problems

Monthly bond maturities for Chinese firms that could struggle to repay

There was also a sign that authorities are looking to expand the state guarantee program, which has tried to boost liquidity for some cash-strapped developers. A top People’s Bank of China official asked state-owned China Bond Insurance Co. in late October to step up support of private developers’ debt issuance. The firm and a key bond-market regulator subsequently met with 21 builders about helping local-note sales, a major state-owned financial newspaper reported.

The latest support step came this week. A PBOC-governed entity--the National Association of Financial Market Institutional Investors--widened a bond financing program to about 250 billion yuan ($34.5 billion) for private companies including real estate firms.

The move is a “big step” to help ease liquidity for top private builders but “not enough to avoid defaults given the still-weak recovery in property sales,” according to Shujin Chen, an equity analyst at Jefferies Hong Kong Ltd.

Provincial Breakdown

Shanghai overtakes Fujian with the most onshore bond defaults this year