When a person or firm makes too much money for too long, it turns heads. And so it was with Steven A. Cohen. Year after year, Cohen's firm, SAC Capital, beat the Street. Big bets, the theory went. Others were not so sure. Big bets generally cut both ways, as many hedge fund managers learned over the years, and even the best in the world, such as John Paulson and Paul Tutor Jones, had their hard times. But such was not the case with Cohen. SAC Capital was the envy of the industry, posting 30 percent annual returns over an 18-year period.

A pattern has emerged. In the world of finance, there are two observable theories that relate to investment performance. The first is reversion to the mean, which simply suggests that market returns tend normalize over time. The second is that the half-life of proprietary trading strategies is short, which simply suggests that however smart a trader is, others will soon pick up on what they are doing and climb on board, suppressing returns over time. If a firm or individual posts market-beating returns year after year, there are generally three possibilities. One, they really are smarter. Two, they are cheating. Or three, they are lying. John Paulson or George Soros are examples of the first category. The Enron group was the second. Bernie Madoff was the third.

We have seen versions of each of these over the years, but in the moment it can be hard to tell which it is. And those involved may not either. Early on in Michael Milken's career, he was clearly one of the smartest guys in the room. He single-handedly created the junk bond industry, and brought new sources of funding to industries that for years had been starved of capital. And he was paid well for his innovation. Only over time did his drive for money and power lead him to cross the line and run afoul of SEC rules.

Steve Cohen was different, apparently. According to a lawsuit filed by his first wife, Cohen funded the creation of SAC Capital from the profits of his first big insider trade, on RCA stock in 1985. When the suit was dismissed, a SAC spokesman suggested that the outcome vindicated Cohen. But a layman's read of the ruling suggests that his wife's claims were denied because the statute of limitations for litigating the purported activities had expired, and the judge never considered the merits of the insider trading claim.

This week, a "remorseful" SAC Capital urged a federal judge to approve a $1.8 billion settlement on charges of insider trading dating back to 1999. To date, Cohen himself has not been convicted of a crime, but he has agreed to close SAC Capital and limit its activities to managing his family's $10 billion investment portfolio.

If one were to believe his scorned first wife, her ex-husband's insider trading activities date back much longer than the period investigated by the SEC, and her claims lead one to wonder if paying a $1.8 billion fine while keeping $10 billion suggests that crime does seem to pay. Cohen, the former Mrs. Cohen would have us believe, might be a really smart guy, but his stellar performance was grounded in illegal activity from the get-go.

A friend in the industry pointed out the problem with the notion that insider trading was only part of Cohen's repertoire. "Once you make that first trade, and realize the outsized returns, it is hard to go back to day trading."

That is the problem as well with high frequency trading (HFT). Michael Lewis has once again explained the arcane to the rest of us in his new book, The Flash Boys, that illuminates the HFT phenomenon. HFT has grown as an industry -- a strategy really -- since its inception less than a decade ago to now account for more than half of the stock trades in the market. HFT is what it sounds like -- lots of very fast trades, where stocks may be bought and then sold in a matter of milliseconds.

HFT has from its inception been the domain of mathematicians and physicists, which led observers to presume that they were in the first category: they were making money because they are that much smarter than the rest of us. But Lewis paints a very different picture: one of an industry corrupted by a pervasive greed that astonishes even the most cynical observer. As detailed by Lewis, the stock exchanges themselves sold -- and continue to sell -- access to information that allows HFT groups tiny timing advantages that essentially allow them to "front-run," or buy stocks in front of investors and sell them to those investors at a slight markup. In essence, it is a modern day version of the old horse racing wire con. They are invisible intermediaries skimming a tiny bit of money off of every trade. Therefore, Lewis' story leads one to conclude that the gross revenues of the HFT industry literally constitute little more than a tax on the portfolios of the rest of the investor universe.

Lewis points out that even the most sophisticated traders -- the SAC Capitals of the world -- had no idea that they were being skimmed. When Lewis' book first came out, a hew and cry welled up in the financial media in defense of HFT, the normal instinct of industry participants to protect their industry from the attacks of the liberal media and others. But after a week or so, those protests gave way to industry participants who realized the enormous damage that HFT has done to the integrity of the industry.

The profit opportunity in what has come to be viewed as computerized front-running essentially undermined any broader market benefits that HFT might theoretically have provided. Defenders of HFT argued it brought "liquidity" to the markets. Liquidity -- assuring that there will be buyers ready to make a bid whenever a seller wants to get out -- is a critical element of effective securities markets. But as quickly became apparent, HFT traders are not providers of liquidity. Rather, their core strategy is built upon getting in the middle of trades that are fairly sure to happen and taking a tiny piece for themselves. If they are providing liquidity, it is only inadvertently, such as when another trader successfully games their system. The other trader might convince the HFT computer that a trade is coming, inducing it to accumulate shares, and then leave the HFT group holding the stock rather than able to turn around and sell it a millisecond later at a profit as intended.

Market observer Jeff Macke emphasized the market manipulation inherent in high frequency trading.

"The trading desks of four different major financial institutions posted gains every single day during the first quarter of 2010. The trading desks of JP Morgan, Bank of America, Citigroup and Goldman Sachs combined posted 244 winning trading days against zero losses. Were the playing field truly level, the odds of a firm making profits or losses on any given day would be roughly 50 percent. The chances of going 61-0 on such a trading field of dreams would be 2.31 quintillion to 1."

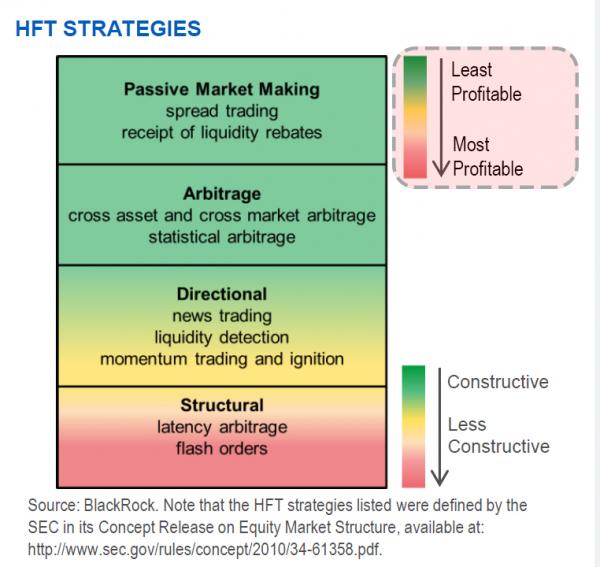

The incomparable Tyler Durden of Zerohedge.com provided this chart encapsulating the problem with HFT. This chart may be Greek to some, but it simply suggests that HFT trading firms are incentivized to migrate from less profitable trading activities that offer some social utility toward more profitable activities that offer little or no social utility. We have seen others go down that road before -- Milken, Enron and mortgage derivatives are prime examples -- and we know exactly where it ends. But as we have seen time and time again, in the moment it is difficult, if not impossible, for market participants to heed those lessons, to voluntarily pull back before things come to a bad end.

As Steve Cohen retires from public view and leaves open questions once again about whether justice has been served, the long-term implications of the emerging story of high frequency trading are yet to be seen. While this may not seem to many to be as significant a moment as the meltdown of complex derivatives five years ago, it certain respects it is a more troubling scandal. By all appearances, actors across the industry -- major banks, the stock exchanges and regulators -- willfully conspired to skim money from individual and institutional investors alike, and few, apparently, were able to step back and see the larger picture of corruption suggested by their collective actions, and the manifest disregard for the public whose interests each are there to serve.