Talking Points:

- The market's favorite volatility measures remain at extremely low levels as risk-oriented assets crawl higher

- There is a natural floor on barometers and assets based on activity levels but not theoretical asset values

- While there is a skew in potential favoring risk aversion, setups more dependent on volatility shift probability

Volatility is a byproduct of risk trends that are prevalent throughout the financial system. Do you have questions on how to better measure or incorporate it into your day-to-day trading? Ask your questions in the Tuesday Trading Q&A which you can register for on the DailyFX Webinar Calendar.

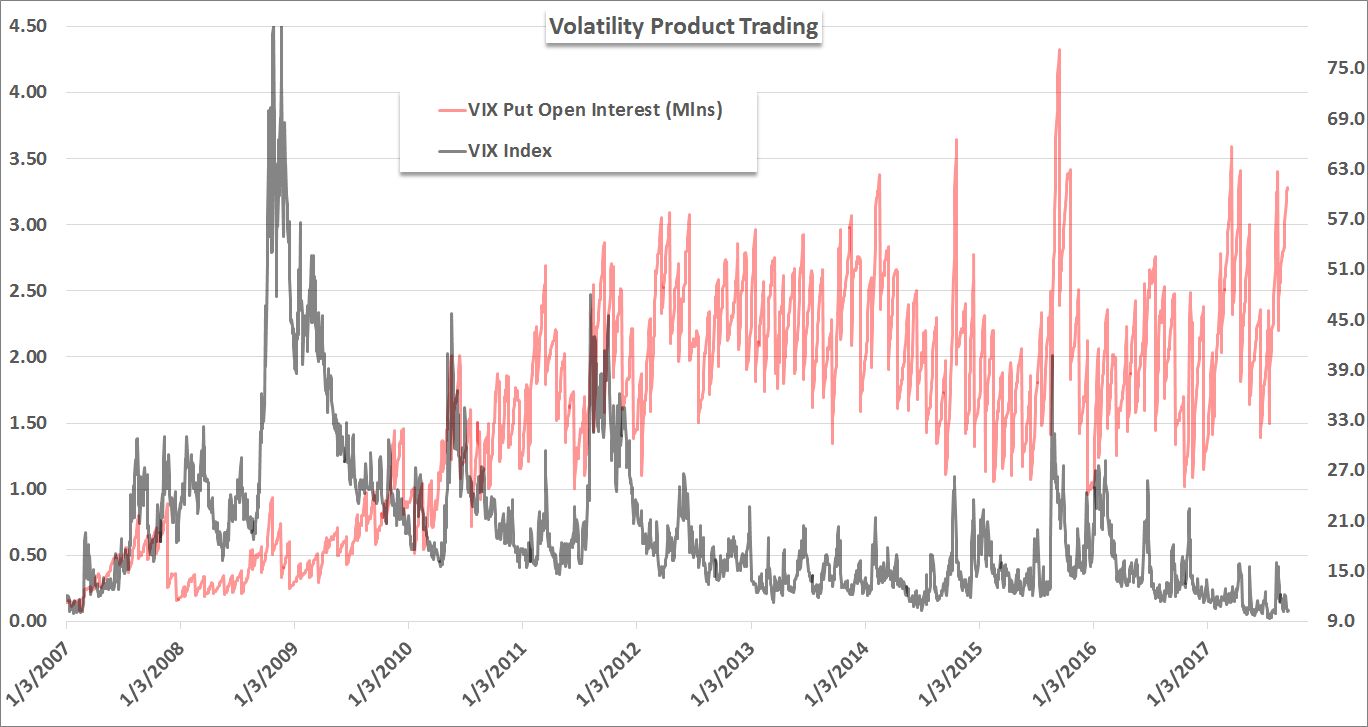

There is no theoretical upper bound to equity prices or index levels, but there is a natural low to volatility. The two are distinctly related with an aversion to risk sending shares and their equivalent sinking while activity measures will rise. That inverse correlation holds for the development in sentiment in the opposite direction. In the financial system market today we find benchmarks like the S&P 500 crawl to fresh record highs on a remarkably consistent basis while conviction to this advance steadily deflates and outright skepticism entrenches. I am dubious of the perfect conditions necessary to make for a productive push reaching for risk returns, but that has been the case for some time. It doesn't pay to fight prevailing trends; but at a certain point, the probability versus potential hits a level such that traders should consider the alternative view on the market.

In measuring trades, before every evaluating the risk-reward of any individual trade; I elevate the potential versus probability of a general view, market or particular asset. These terms are too often used interchangeably but they are in fact very different measures. The probability of a development - as one would assume - is the likelihood that it will happen. The probability that the S&P 500 continues higher for example is higher than the chance that it falls. That can be assessed by momentum, capital inflows and other practical measures. Yet, how far and how fast will this market advance. Given years of climb to further and further record highs with so much idle and 'safe' capital pushed to this risky asset, the tempo is unlikely to persist. Alternatively, the probability that the benchmark US index falls is lower given the prevailing momentum, but the one-sided nature of the market suggests that the deleveraging and interest in volatility should it turn would likely entail a far more remarkable ('potential' laden) scenario.

So, how do we take advantage of the skew between potential and probability given the persistence of complacency and a lack of natural ceiling in popular assets? Those trades more distinctly connected to volatility can offer the better probability-potential balance - by either lowering the cost or increasing the sensitivity to modest risk aversion. This could theoretically be employed to assets with a mere high sensitivity to speculative fluctuation, but I would set the highest requirements to such trades as they come to close to 'picking tops'. Technical breaks that show progress in reversing extreme exposure and/or clear fundamental drive to override sentiment are the best means for shifting the probability measure. More appealing are the assets that can more directly cater to the potential to further offset the unfavorable probability. Volatility measures with their natural lower bounds do this well. Yet, the popular XIV and VXX come with clear limitations. VIX futures are arguably more uniquely suited to this view. And, as a trader who started out in options, the important pricing feature of implied volatility can blend this imbalance with unique contributing features of a preferred market (indexes, currency, junk bond, gold, etc). We focus in on volatility and its trade implications in today's Quick Take video.

To receive John’s analysis directly via email, please SIGN UP HERE.