Financial markets: Calm before the storm?

- Published

Just like Baby Bear's porridge, there's a feeling in the financial markets that things are neither too hot, nor too cold.

All the indicators are telling us that the temperature is just right.

Stock markets have steadily climbed to new records, but haven't seen such low volatility for years.

Daily stock market movements of, say, more than 1%, have been pretty rare recently among the leading indexes.

It's a similar story in the currency, bond and commodity markets.

A few years ago, a rebel attack on Iraq's oilfields would have jolted the crude price sharply higher. Not now. Despite the small oil price rise over Iraq tensions, crude volatility is at historic lows.

In Spain, whose economy was for so long a byword for crisis and turmoil, the government can now borrow money at rates similar to those in the UK. Across Europe's periphery economies, bond yields have fallen sharply as risk capital returns to the markets.

A contentment seems to have descended. Sharp deviations in prices - that is, volatility - are a thing of the past.

No fear, no worries

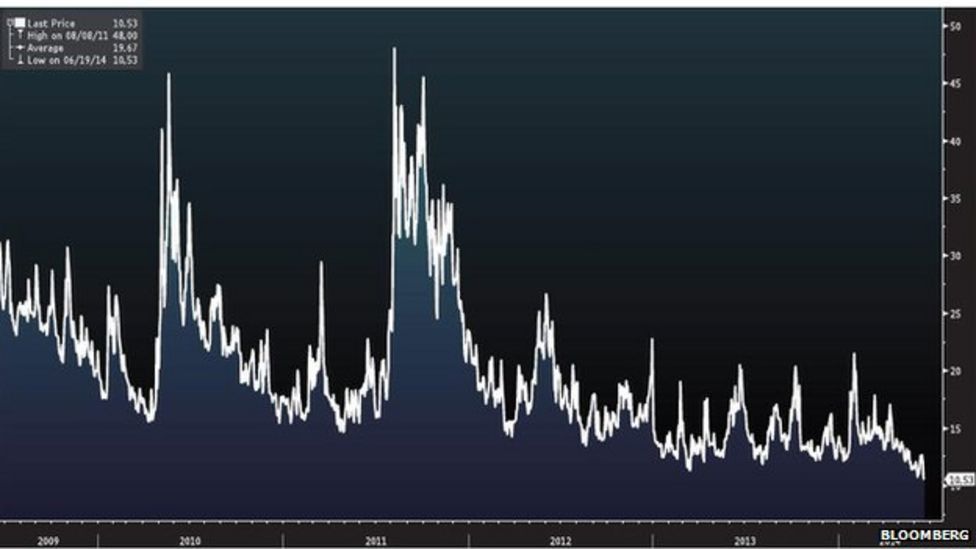

The relaxed attitude is summed up in the so-called 'fear index'. The Vix, a measure of implied market volatility on Wall Street, is at a seven-year low.

Meanwhile, Euro STOXX Volatility Index, another measure of stock market risk aversion, fell to its lowest since December 2006 on Thursday.

Great news? Not necessarily. There's a concern among monetary officials and economists that investors are being lulled into a false sense of security.

Says Ryan Sweet, senior economist at Moody's Analytics: "Bond market volatility is very low. Stock market volatility is very low. So any sudden spike in volatility could cause interest rates to rise very sharply."

In short, the worry is that years of low interest rates and central bank intervention has encouraged investors to take ever-greater risks, and take on more debt in the process. But history shows that risk-taking frequently ends in tears.

Low volatility preceded the 2007 crash, and the 1997 Asian financial crisis. Historians say it was also evident before the 1929 Wall Street slump.

The head of the International Monetary Fund, Christine Lagarde, warned last week about complacency in the financial markets.

On Wednesday, the head of the US Federal Reserve, Janet Yellen, went further. She said: "The extent that low levels of volatility may induce risk-taking behaviour that, for example, entails excessive build-up in leverage or maturity extension - things that can pose risks to financial stability later on - is a concern to me."

The economist George Magnus says that the seemingly benign attitude has similarities to the Great Moderation - a term used to describe the years before the last financial crash, when some people predicted the end of boom and bust, and regarded stability as the new norm.

'Calm before the storm'

"The previous Great Moderation ended in great volatility: this one may well do so too," Mr Magnus wrote in a research paper earlier this month.

"The Great Moderation was a nirvana for financial institutions and investors. It was learned at great cost that this had been a fantasy world... leading to an eventually catastrophic outcome," he said.

The concern is that low rates and economic stimulus are masking inherent instabilities. Economic and geo-political risks remain, and in some cases are rising.

The eurozone's problems have not gone away, and there is a slowdown in China's economy and across Asia; interest rates are set to rise, and markets must adjust to an era without governments' stimulus programmes.

These, and other concerns, may yet spark a sudden stock market correction, increase worries about the quality of some government or corporate bonds, and a tumble in other asset prices.

Mr Magnus describes the current market "tranquillity" as possibly just the "calm before the storm".

Yet, perhaps the fundamentals are correct. Recovery in some countries - especially the US and UK - looks entrenched. Job creation and wages are growing slowly, but steadily.

Companies are making profits and increasing dividends. Around the world, financial regulators are weeding out the sort of trading practices and off-balance sheet engineering that create instability.

Obviously, too much volatility is bad. Investors panic; many cut their losses and run. But recent comments from central bankers suggest that they are alive to the risk of applying the brakes too soon with rapid rises in interest rates.

Unchartered territory

So, is possible that financial markets are simply adjusting to reflect this new economic reality, rather than being complacent?

Edward Hadas, economics editor at the commentary website Breakingviews, believes that the world economy is in unchartered territory - so no one really knows what might happen.

"We are dealing with something we have never seen before: very low volatility in such uncertain economic times," he says.

Low volatility is supposed to imply calm and confidence. But he sees no evidence that investors are not aware of the global economic risks. In the media and among the commentariat in the City, there are plenty of warnings that challenges remain.

Mr Hadas wonders if the low volatility is due to more mundane factors: the banks that provide most of the funding for traders are under capital pressure.

"The result is less activity, less volatility and a greater correspondence of markets with reality," he said.

But he warns: "Sadly, the calm is probably temporary. Traders will re-group and become more active once they adjust to the new funding environment. And whenever economic reality does change sharply, investors can be counted on to overreact."

- Published19 June 2014