In the last post I wrote, I mentioned that I recently moderated a global webinar for financial advisors on the topic of S&P DJI research on passive vs active. We received 20 questions during the course of this webinar. I thought that it would be interesting to share some of those questions from advisors and the answers that our panelists provided. The replay of the webinar is available if you missed it.

Question: To what extent does using S&P DJI’s proprietary indices affect the outcome of the SPIVA studies?

Answer from Aye Soe, Global Head of Index Research & Design at S&P Dow Jones Indices: That certainly does matter. A great example of how much it can matter is in the U.S. Smallcap space. In research we recently published, we found that the S&P SmallCap 600 outperformed the Russell 2000 Index by 172 bps per annum between 1994 and 2014. This example shows the importance of benchmark selection.

Question: How could the SPIVA results change if you stripped out the closet indexers and only looked at truly active managers?

Answer from Rick Ferri, Founder and Managing Partner of Portfolio Solutions: We did not attempt to define what a closet indexer was or separate those funds from other actively managed funds.

Answer from Aye Soe: We use the University of Chicago’s Center for Research in Security Prices (CRSP) Survivorship Bias Free Mutual Fund Database. Our goal is to provide an “apples to apples” comparison in size, style, and other characteristics to compare indices to mutual funds. Active share and closet Indexing are topics which seem to be getting more analytical attention, but closet indexers is not a strong definition or classification that we have yet incorporated into our research.

Question: Is “alpha” a myth? (Since by definition index funds can’t achieve positive alpha)

Answer from Aye Soe: SPIVA and Persistence, when used together show how difficult “alpha” is to deliver and sustain. So it isn’t a myth but it might be described as rare.

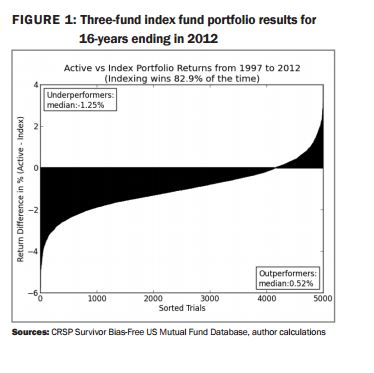

We did not have time to answer all the questions we received during the webinar. I followed up with our three presenters and then personally emailed consolidated answers from our presenters to each person who sent in a question. I want to conclude by emphasizing that all three of our presenters made the point (which is documented in our Persistence Scorecard research) that past delivery of alpha is no guarantee of future delivery. Rick questioned whether taking the chance in selecting active managers is a good bet. He showed data on the median of outperformance and the median of underperformance indicating a negative skew. Here is one graph from Rick’s study that shows this skew: